The collection industry continues to respond to a changing consumer landscape with innovative and technological solutions to drive efficiencies while mitigating risk. Sometimes both can be achieved by relying on deep industry experience and “knowing where the acorns are buried” within your current process.

In the back corners of creditor collection systems are categories of accounts that are unpaid but alas, do not receive any further collection effort. Consumers have invoked their rights to request “no further contact” or directed the creditor to “communicate only with my designated representative.” At the time, these accounts were property coded by the creditor and taken out of the standard collection path into a specialized handling strategy that often ends with the debt still due. There are three common categories for these accounts that require specialized handling as follows:

- Cease & Desist

- Debt Settlement Agency

- Attorney Representation

Harvest Strategy Group has extensive experience with each of these and can create a litigation recovery program to effectively handle them in a compliant manner. Larger creditors can add thousands of charged-off accounts to these categories monthly, creating significant recovery opportunity if handled correctly. It is our experience that when compared to standard inventory, each of these three categories can be more collectable from a liquidation standpoint than other accounts.

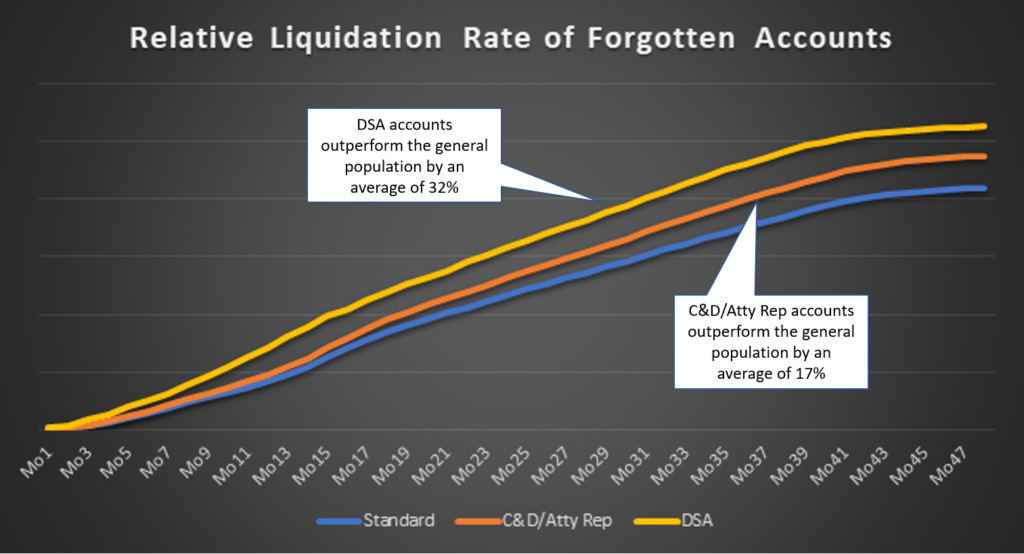

How do forgotten accounts perform, relative to the general population?

From a collection perspective, it is our experience that the liquidation rate from accounts in these categories is at least the same and often higher than other charged off accounts. Theories abound as to why they are often more collectable, but we hypothesize it is based on the following factors:

- Cease & Desist requests are often not collected by creditors because recovery through litigation is the only option. If the creditor does not employ a litigation program or does not include C&D inventory in that program, the consumer has put up an effective wall between themselves and all their creditors. Filing suit breaks through that wall.

- Debt settlement agencies require a source of income to be enrolled, and these individuals are more likely to be employed than those in the general population of charged off accounts and are therefore more collectable, particularly through judgment enforcement.

- Attorney representation usually requires a down payment or retainer unless it is obtained from one of the pro bono public service agencies. Often times the representation by the attorney ends but the “attorney represented” flag still remains in the creditor’s system. Like Cease & Desist, if there is no program to effectively handle these accounts by the creditors then the consumer has effectively ended collection activity until the statute of limitations expires and then litigation is no longer an option.

It is important to note that the law provides protection to consumers for these specialized categories of accounts and only collectors/paralegals who are specifically trained in the handling of these accounts should be utilized to ensure consumer’s rights are upheld. If the consumer responds to collection efforts, listening and understanding is critical for these accounts. There could be legitimate issues that need to be addressed which underpin the reason the account was put into one of these statuses in the first place. As with any account, any allegations should be investigated with the creditor before proceeding with additional recovery efforts.

Below is a chart showing actual comparative recovery data for each of these types of accounts as compared to the general population of accounts (similar accounts that have not invoked one of these options).

In summary, collection and recovery programs are only increasing in complexity given the increasing number of marketplace services and changing State and Federal laws. Taking time to design a compliant process that respects consumer rights and treats each account according to its unique characteristics is an ongoing process that is necessary for proper portfolio management. Instituting a litigation recovery program specifically designed to deal with these important categories of accounts can significantly improve recovery results and assist consumers with resolving these accounts. Contact us to learn more about the specific processes we have designed to maximize recovery of these often forgotten accounts.

Harvest Strategy Group, Inc. (Harvest) is a recognized leader in national accounts receivable management services, delivering best-in-class results for the nation’s largest banks, finance companies and credit unions. Harvest’s mission is to execute custom recovery programs on behalf of its clients to maximize revenue, while protecting their brand with proven regulatory compliance and vendor oversight processes. Harvest’s leading recovery performance is fueled by ProScoreTM, its proprietary portfolio scoring and segmentation model. For more information, visit www.harveststrategygroup.com or call Jamie Welsh at (303) 531-0654.